Nearly 1.6 million members of the military community have an important decision to make before the end of this month: whether to opt into the Blended Retirement System (BRS). Kate Horrell, an expert on military personal finance issues, explains how the BRS differs from the old retirement system and why you need to make an informed decision about which retirement system you choose.

Nearly 1.6 million members of the military community have an important decision to make before the end of this month: whether to opt into the Blended Retirement System (BRS). Kate Horrell, an expert on military personal finance issues, explains how the BRS differs from the old retirement system and why you need to make an informed decision about which retirement system you choose.

Being able to use Space-A travel benefits is awesome. If you plan to fly Space-A during your retirement, you’re going to need time to travel (because we all know that Space-A isn’t always the fastest way to get somewhere). Making time to travel is a lot easier if you’ve organized your retirement finances so that you aren’t tied to a full-time job to pay the monthly bills.

And that’s exactly why I’m writing this post about the military’s new Blended Retirement System (BRS) for a travel website.

Does BRS Affect You?

Let’s start by reviewing who isn’t affected by the changes to the military’s retirement system.

If you’re already retired, nothing is changing. If you had more than 12 years service (or 4320 reserve points) on 31 December 2017, nothing is changing. And if you’re brand-new to the military, joining since 1 January 2018, you’re automatically enrolled in the BRS.

That leaves us with a huge number of folks, approximately 1.6 million, who joined the military before 1 January 2018 but had less than 12 years of service (4320 reserve points). This group remains in the old legacy retirement system but has the option to choose BRS.

> > The window to switch retirement plans ends this month, on 31 December 2018.

If you fall into that group, you’ve got to find some time this busy month to learn everything you can about BRS and make a thoughtful, educated decision about which system is better for you. The decision is final. Unlike with health insurance, you do not have an annual window to change which retirement system you’re enrolled in.

The Three Main Ways BRS is Different

There are three important ways that BRS differs from the legacy retirement system: government contributions to your Thrift Savings Plan (TSP) account; a smaller military retirement paycheck; and mid-career continuation pay.

Government Contributions to TSP

Under the legacy retirement system, there is no government contribution to your TSP account.

The big draw of BRS is the government-provided retirement money (in the form of contributions to your TSP), whether you serve for one term or a full career.

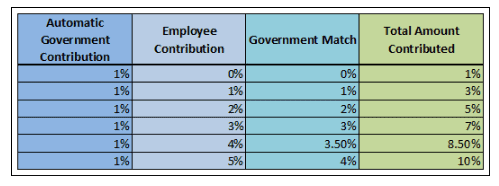

There are two components to what the government gives you: automatic government contributions and government match of your TSP contributions.

The government contribution equals 1% of your base pay and is contributed beginning at 60 days of service. You get this money whether you contribute to TSP or not. This money is yours to take with you once you’ve served for 2 years.

The government matching is up to 4% for a 5% service member contribution to TSP. (The first three percent are matched at 100%, and the fourth and fifth percent are matched at 50%.) The government starts matching your TSP contributions after 24 months of service. Your contributions are always yours, and government matching funds are yours immediately.

The table below illustrates how these contributions add up:

Together, the government contribution and government match mean that you can get a government contribution of up to 5% of your base pay if you contribute 5% of your base pay to your TSP account. That can add up to a lot of money that remains yours, even if you don’t earn a military retirement paycheck.

Together, the government contribution and government match mean that you can get a government contribution of up to 5% of your base pay if you contribute 5% of your base pay to your TSP account. That can add up to a lot of money that remains yours, even if you don’t earn a military retirement paycheck.

Military Retirement Pay

Under the legacy retirement system, your military retirement pay is calculated by multiplying your years of service by the average of your highest 36 months’ pay by 2.5. Therefore, at 20 years of service, your military retirement pay is 50% of your high-36 average.

Legacy Retirement System Retirement Pay Calculation for 20 Years of Service:

(Years of Service) x (Avg of Highest 36 Months’ Pay) x 2.5 = 50% of High-36 Avg

Under the BRS, your military retirement pay is calculated by multiplying your years of service by the average of your highest 36 months’ pay by 2.0. Therefore, at 20 years of service, your military retirement pay is 40% of your high-36 average.

BRS Retirement Pay Calculation for 20 Years of Service:

(Years of Service) x (Avg of Highest 36 Months’ Pay) x 2.0 = 40% of High-36 Avg

It’s important to remember that a relatively small percentage of military service members will earn a retirement paycheck — less then 20%. Even if you’re already at 12 years of service, there is still a greater than 15% chance that you won’t make it to retirement.

If you remain in the legacy system and don’t get to retirement, you will leave the military with no retirement funds except your own contributions to the TSP.

Continuation Pay

Continuation pay is a one-time mid-career payment, like a bonus, paid in return for the agreement to serve for an additional period of time.

The legislation on continuation pay gives the branches pretty wide latitude in the timing and amount of continuation pay, but it will be given between 8 and 12 years of service, and the amount can range from 2.5 to 13 times monthly basic pay for active duty service members, and 0.5 to 6 times monthly basic pay (based on active duty pay charts) for National Guard or reserve in a drilling status.

For 2018, all the branches (except the Public Health Service) selected the same details for Continuation Pay: 2.5% monthly pay for active duty, 0.5% monthly pay for reserve and National Guard, to be paid at 12 years of service, with an additional 4 year obligation. The Public Health Service offered the same amounts and obligation at 10 years of service.

The government has not yet released 2019 rates, but if they once again offered Continuation Pay of 2.5% at 12 years of service, that would equate to $9,142 for an E-6 or $18,090 for an O-4.

Which Retirement Plan is Right for You?

So, how do you decide which retirement plan is right for you? There is definitely no single right answer – everyone’s situation is different.

Generally speaking, if you have any inkling that you might not want to serve for a full career, you should switch to BRS. BRS gives you government contributions to your retirement without earning a military retirement check.

Keep in mind that even those who think they’ll stay for 20 years often find themselves getting out unexpectedly, whether they have a family situation, or they can’t maintain their physical standards, or there is a reduction in forces, or there is a health crisis, or they get a DUI.

A study from the Rand National Defense Institute shows that 84% of new enlisted service members and 50% of new officers won’t make it to retirement. While those percentages decrease with each year of service, even with 12 years in, 19% of enlisted and 15% of officers get out of the military before retirement.

However, if you’re at 12 years, and you’re already committed to staying for another handful of years, and your family loves the military, and you’re in great health, then maybe the legacy system is a good gamble for you.

Can’t Decide? Get Free Help Analyzing Your Options

Once you’ve done all your research, if you still can’t decide, it might be worth talking this out with a financial educator at your installation’s family service center.

They go by different names: personal financial manager, personal financial specialist, etc., but they all do the same thing. They won’t tell you what choice is right for you, but they will help you think through the various options.

You can also learn more about the details of the BRS in the many resources listed in 50+ Places To Learn About The Military’s New Blended Retirement System.

Make An Informed Decision

No matter what you decide, the most important part is that you make an educated, thoughtful choice before the 31 December 2018 deadline whether to opt into BRS. Taking no action at all is a choice to stay in the legacy system – which is fine as long as that is your informed decision.

Once again, remember that you have only a small window to make this choice, and you cannot change your decision later.

The BRS is a great opportunity for all eligible service members to receive government contributions to their TSP account. Only you can decide whether that’s worth the smaller retirement paycheck if you make it to retirement. Learn the details and make a decision before the deadline!

***

Kate Horrell is a Navy spouse and personal financial educator who works with military and veteran families to make the most of their pay and benefits. You can find her at KateHorrell.com.